Determining whether a worker is an employee or contractor depends on the nature of the working arrangement not the label given to the worker.

It is possible for an independent contractor to be deemed an employee even where the contractor has been issuing tax invoices.

There is no statutory definition of employment. In determining whether a worker is an employee or a contractor there are a series of questions to be asked which address the different aspects of the relationship between the hirer and the worker who is supplying the labour.

The questions address the degree and nature of control exercised over the worker, the mode of remuneration, responsibility, the provision and maintenance of tools or equipment, the extent of the obligation to work and the capacity to delegate work.

The greater the control the more likely it is that the worker will be an employee. However, control is only one aspect of the relationship. A court will examine the ‘totality of the relationship’ in determining whether a worker is an employee or contractor.

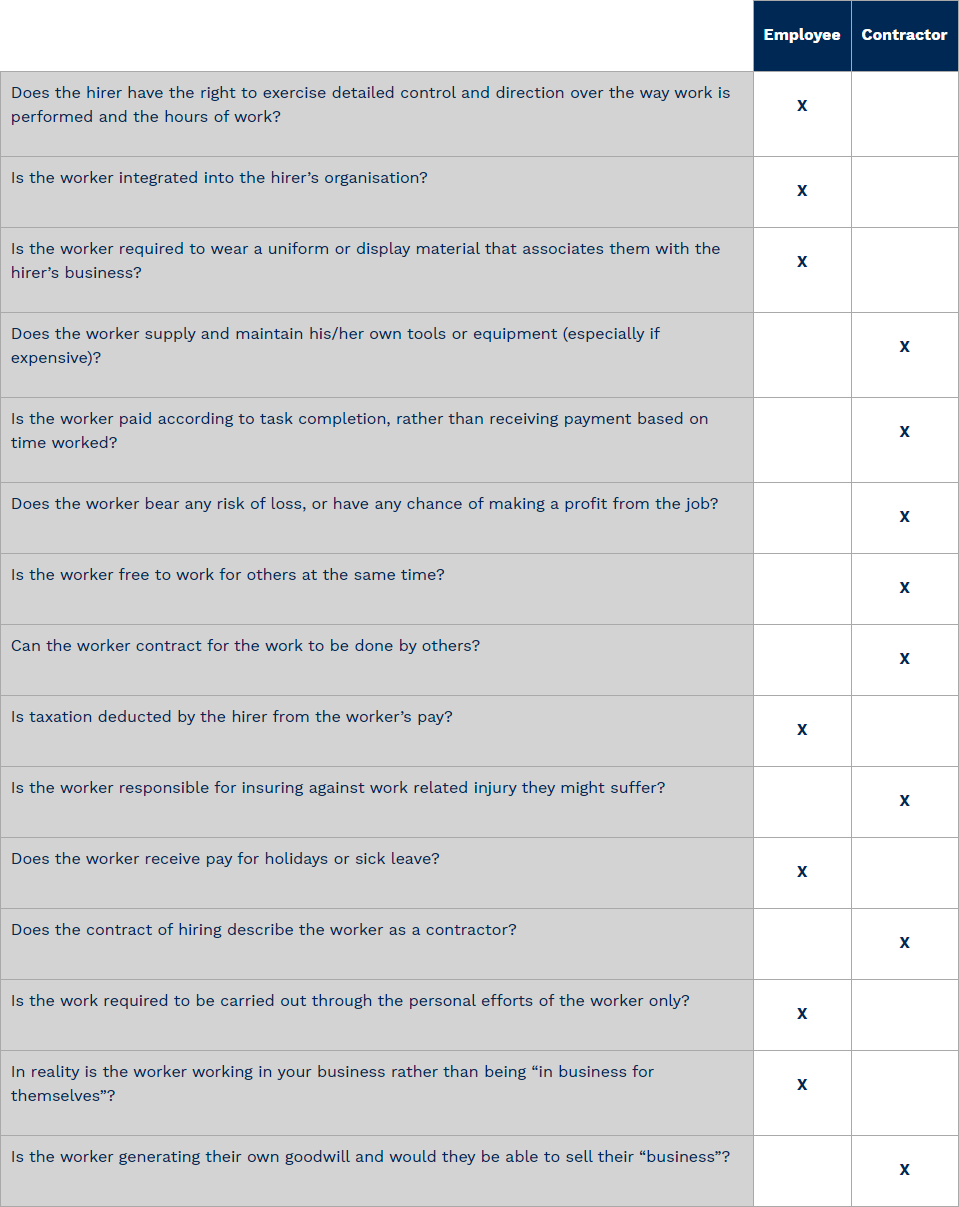

Some of the significant questions a court would address in determining whether a worker is an employee or contractor are set out in the table below. (a “yes” answer to the question posed is indicated by the “cross”):

The above table is not a comprehensive list to determine whether a worker is an employee or a contractor, however, it indicates some of the significant issues a court would look at in determining whether a worker is an employee or a contractor.

There is no definitive decision on whether a worker is an employee or contractor; courts will determine each case on its own set of facts.

Relatively recent decisions on this issue have been decided both ways.

Workers Deemed Employees

Some examples of cases where workers have been found to be employees are as follows:

Hollis v Vabu (2001) – bicycle courier who was paid according to the number of successful deliveries, but who had to wear the company uniform, was told when to work and how much to charge, and did not have to supply expensive equipment.

Roy Morgan Research v Commissioner of Taxation (2010) – market research interviewers who could accept or reject assignments to perform work but were subject to detailed rules as to how they conducted interviews.

Victorian WorkCover v Game (2007) – Mr Game operated as an independent contractor performing bricklaying and other work under a contract for services. He was paid a daily rate by a builder. The court held that this did not rule out the possibility that on this particular occasion, when Mr Game and his colleagues agreed to fill in for someone else and dig trenches after completing a bricklaying job that he had been hired as an employee.

ACE Insurance Limited v Trifunovski [2013] – the full Federal Court held five sales agents were employees despite signing contracts that said they were independent contractors. Two of the agents were engaged through a corporate entity. Important elements in reaching the decision were:

- that the agents were the representatives of the insurance company; and

- that the insurance company had a right to control the work of the agents.

The decision resulted in the insurance company being ordered to pay more than $500,000 in accrued annual leave and long service leave.

Justice Buchanan, with whom Justices Lander and Robertson agreed, analysed the dismissal of the agents.

Justice Buchanan held it was critical to the engagement that the sale of insurance was required to be undertaken by the personal efforts of the individual agents only.

Justice Buchanan said [at 148]:

“The overwhelming impression from the evidence is that the agents at each of the three levels were specifically trained by [the company] in particular techniques of selling which [the company] had adopted as its own, and the training was constantly reinforced. They then worked under close direction, supervision and organisation with a view to selling insurance products in a way determined by [the company]. They had no real independence of action or true independence of organisation. Once the mutual representation, that the agents were not employees, was set to one side there was no adequate foundation for a conclusion that the relationship was anything other than one of employment. The representation did not suffice to make it one.”

The court rejected the insurance company’s argument that the engagement of two of the agents through a corporate entity was decisive. Justice Buchanan stated [at 135]:

“These contracts were made with individual agents. The agent was the authorised seller, no-one else. What was assignable to a corporation were” rights and benefits” under the contract. The trial judge inclined to the view that this merely permitted channelling of income to a corporate vehicle. The right to engage in other business was subordinated to the personal obligations owed by the agents to [the company]. Permission to engage staff did not amount to a power of delegation.”

Workers Deemed Contractors

By contrast, the courts have held workers are contractors rather than employees in the following cases:

Australian Air Express v Langford (2005) – delivery driver who worked under arrangements similar to the courier in Hollis v Vabu, but was required to own and supply an expensive truck, and was able to substitute another driver with the delivery company’s approval.

Sweeney v Boylan Nominees (2006) – refrigeration mechanic, who supplied his own tools and equipment, invoiced for each job he did and was required to maintain his own insurance.

ACT Visiting Medical Officers v AIRC (2006) – doctors who worked in a hospital and also treated private patients as part of an independent business were held not to be employees in relation to the public patients they saw as that work was an integral part of their practice.

Commissioner of State Revenue v Mortgage Force Australia (2009) – ‘consultants’ engaged by a finance broker to act as its agents in processing applications for finance, under contracts that gave them considerable discretion as to how and when they rendered their services and allowed them (with the consent of the broker) to appoint sub-agents in their place.

As you will note from the above brief outline of cases, this area of the law is unsettled.

Conclusion

The key consideration is the totality of the working arrangement, including the performance of work under the control and direction of the employer. Taxation arrangements, annual leave and personal/carers (sick) leave, pay rates and workers compensation arrangements are only indicators of a particular type of arrangement. They do not independently determine whether a worker is an employee or a contractor.

Employers must be very careful to ensure that workers engaged as contractors are truly contractors. If a worker is deemed an employee, the employer may be liable for payment of entitlements such as holiday pay, personal/carers entitlements, long service leave, overtime and other award allowances.

About the Author